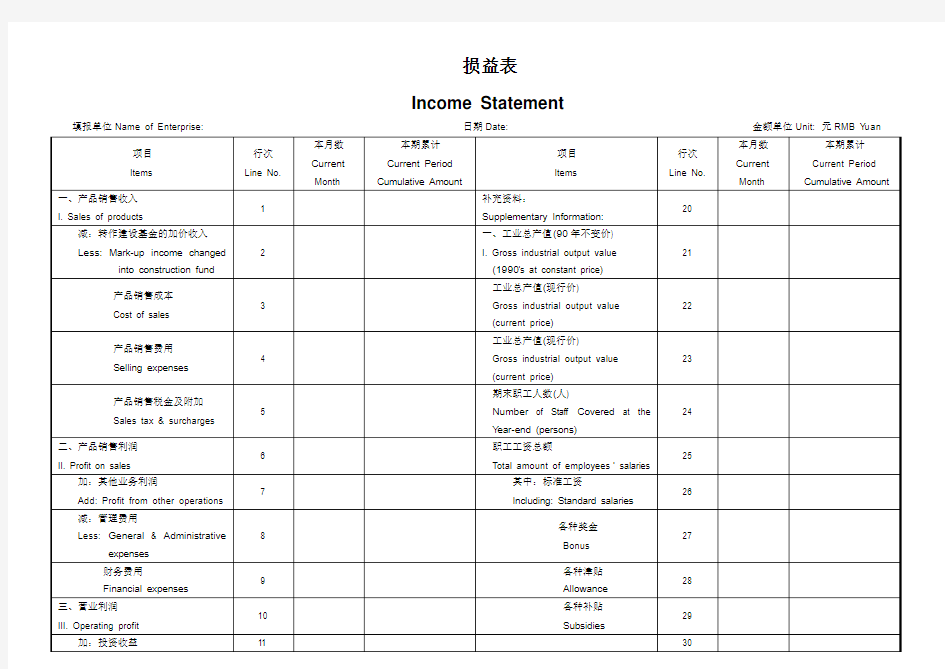

损益表_模板(中英对照)

损益表

Income Statement

填报单位Name of Enterprise: 日期Date: 金额单位Unit: 元RMB Y uan

单位负责人Person in Charge of the Enterprise: 主管会计工作负责人Person in Charge of Accounting:

总会计师Chief Accountant: 制表Tabulated by:复核Check:

企业资产负债表_利润表中英文对照大全

资产负债表Balance Sheet 项目ITEM 货币资金Cash 短期投资Short term investments 应收票据Notes receivable 应收股利Dividend receivable 应收利息Interest receivable 应收帐款Accounts receivable 其他应收款Other receivables 预付帐款Accounts prepaid 期货保证金Future guarantee 应收补贴款Allowance receivable 应收出口退税Export drawback receivable 存货Inventories 其中:原材料Including:Raw materials 产成品(库存商品) Finished goods 待摊费用Prepaid and deferred expenses 待处理流动资产净损失Unsettled G/L on current assets 一年内到期的长期债权投资Long-term debenture investment falling due in a yaear 其他流动资产Other current assets 流动资产合计Total current assets 长期投资:Long-term investment: 其中:长期股权投资Including long term equity investment 长期债权投资Long term securities investment *合并价差Incorporating price difference 长期投资合计Total long-term investment 固定资产原价Fixed assets-cost 减:累计折旧Less:Accumulated Dpreciation 固定资产净值Fixed assets-net value 减:固定资产减值准备Less:Impairment of fixed assets 固定资产净额Net value of fixed assets 固定资产清理Disposal of fixed assets 工程物资Project material 在建工程Construction in Progress 待处理固定资产净损失Unsettled G/L on fixed assets 固定资产合计Total tangible assets 无形资产Intangible assets 其中:土地使用权Including and use rights 递延资产(长期待摊费用)Deferred assets 其中:固定资产修理Including:Fixed assets repair 固定资产改良支出Improvement expenditure of fixed assets 其他长期资产Other long term assets 其中:特准储备物资Among it:Specially approved reserving materials 无形及其他资产合计Total intangible assets and other assets

英文损益表

Income statement and profit appropriation 一、主营业务收入Revenue 减:主营业务成本Less: Cost of Sales 主营业务税金及附加Sales Tax 二、主营业务利润(亏损以“—”填列)Gross Profit ( - means loss) 加:其他业务收入Add: Other operating income 减:其他业务支出Less: Other operating expense 减:营业费用Selling & Distribution expense 管理费用G&A expense 财务费用Finance expense 三、营业利润(亏损以“—”填列)Profit from operation ( - means loss) 加:投资收益(亏损以“—”填列)Add: Investment income 补贴收入Subsidy Income 营业外收入Non-operating income 减:营业外支出Less: Non-operating expense 四、利润总额(亏损总额以“—”填列)Profit before Tax 减:所得税Less: Income tax 少数股东损益Minority interest 加:未确认投资损失Add: Unrealised investment losses 五、净利润(净亏损以“—”填列)Net profit ( - means loss) 加:年初未分配利润Add: Retained profits 其他转入Other transfer-in 六、可供分配的利润Profit available for distribution( - means loss) 减:提取法定盈余公积Less: Appropriation of statutory surplus reserves 提取法定公益金Appropriation of statutory welfare fund 提取职工奖励及福利基金Appropriation of staff incentive and welfare fund 提取储备基金Appropriation of reserve fund 提取企业发展基金Appropriation of enterprise expansion fund 利润归还投资Capital redemption 七、可供投资者分配的利润Profit available for owners' distribution 减:应付优先股股利Less: Appropriation of preference share's dividend 提取任意盈余公积Appropriation of discretionary surplus reserve 应付普通股股利Appropriation of ordinary share's dividend 转作资本(或股本)的普通股股利Transfer from ordinary share's dividend to paid in capital 八、未分配利润Retained profit after appropriation 补充资料:Supplementary Information: 1.出售、处置部门或被投资单位收益Gains on disposal of operating divisions or investments 2.自然灾害发生损失Losses from natural disaster 3.会计政策变更增加(或减少)利润总额Increase (decrease) in profit due to changes in accounting policies 4.会计估计变更增加(或减少)利润总额Increase (decrease) in profit due to changes in accounting estimates 5.债务重组损失Losses from debt restructuring

会计英语资产负债表及利润表

会计报表中英文对照

Accounting

1.Financial reporting(财务报告) includes not only financial statements but also other means of communicating information that relates, directly or indirectly,to the information provided by a business enterprise’s accounting system----that is,information about an enterprise’s resources, obligations, earnings,etc. 2.Objectives of financial reporting:财务报告的目标 Financial reporting should: (1) Provide information that helps in making investment and credit decisions. (2) Provide information that enables assessing future cash flows. (3) Provide information that enables users to learn about economic resources, claims against those resources, and changes in them. 3. Basic accounting assumptions 基本会计假设 (1) Economic entity assumption会计主体假设 This assumption simply says that the business and the owner of the business are two separate legal and economic entities. Each entity should account and report its own financial activities. (2) Going concern assumption 持续经营假设 This assumption states that the enterprise will continue in operation long enough to carry out its existing objectives. This assumption enables accountants to make estimates about asset lives and how transactions might be amortized over time. This assumption enables an accountant to use accrual accounting which records accrual and deferral entries as of each balance sheet date. (3) Time period assumption 会计分期假设 This assumption assumes that the economic life of a business can be divided into artificial time periods. The most typical time segment = Calendar Year Next most typical time segment =Fiscal Year (4) Monetary unit assumption 货币计量假设 This assumption states that only transaction data that can be expressed in terms of money be included in the accounting records,and the unit of measure remains relatively constant over time in terms of purchasing power. In essence,this assumption disregards the effects of inflation or deflation in the economy in which the entity operates. This assumption provides support for the "Historical Cost" principle. 4.Accrual-basis accounting 权责发生制会计 5.Qualitative characteristics 会计信息质量特征 (1) Reliability可靠性 For accounting information to be reliable,it must be dependable and trustworthy. Accounting information is reliable to the extend that it is: Verifiable:means that information has been objectively determined,arrived at, or created.More than one person could consider the facts of a situation and reach a similar conclusion.

三大会计报表:资产负债表、损益表、现金流量表中英文对照

英文会计报表:FINANCIAL REPORT COVER 报表所属期间之期末时间点Period Ended 所属月份Reporting Period 报出日期Submit Date 记账本位币币种Local Reporting Currency 审核人Verifier 填表人Preparer 所属月份Reporting Period 报出日期Submit Date 资产负债表 Balance Sheet Assets Current Assets Bank and Cash Current Investment 一年内到期委托贷款Entrusted loan receivable due within one year 减:一年内到期 Less: Impairment for Entrusted loan receivable due within one year 减: Less: Impairment for current investment Net bal of current investment Notes receivable Dividend receivable 应收利息Interest receivable Account receivable 减:应收账款 Less: Bad debt provision for Account receivable Net bal of Account receivable Other receivable 减:其他应收款坏账准备Less: Bad debt provision for Other receivable 其他应收款净额Net bal of Other receivable Prepayment Subsidy receivable Inventory 减: Less: Provision for Inventory 存货净额Net bal of Inventory 已完工尚未结算款Amount due from customer for contract work Deferred Expense 一年内到期的 Long-term debt investment due within one year 一年内到期的应收融资租赁款Finance lease receivables due within one year Other current assets Total current assets 长期投资Long-term investment Long-term equity investment 委托贷款Entrusted loan receivable

利润表中英文对照版

利润表中英文对照版 一、主营业务收入Revenue 减:主营业务成本Less: Cost of Sales 主营业务税金及附加Sales Tax 二、主营业务利润(亏损以“—”填列) Gross Profit ( - means loss) 加:其他业务收入Add: Other operating income 减:其他业务支出Less: Other operating expense 减:营业费用Selling & Distribution expense 管理费用G&A expense 财务费用Finance expense 三、营业利润(亏损以“—”填列) Profit from operation ( - means loss) 加:投资收益(亏损以“—”填列) Add: Investment income 补贴收入Subsidy Income 营业外收入Non-operating income 减:营业外支出Less: Non-operating expense 四、利润总额(亏损总额以“—”填列) Profit before Tax 减:所得税Less: Income tax 少数股东损益Minority interest

加:未确认投资损失Add: Unrealised investment losses 五、净利润(净亏损以“—”填列) Net profit ( - means loss) 加:年初未分配利润Add: Retained profits 其他转入Other transfer-in 六、可供分配的利润Profit available for distribution( - means loss) 减:提取法定盈余公积Less: Appropriation of statutory surplus reserves 提取法定公益金Appropriation of statutory welfare fund 提取职工奖励及福利基金Appropriation of staff incentive and welfare fund 提取储备基金Appropriation of reserve fund 提取企业发展基金Appropriation of enterprise expansion fund 利润归还投资Capital redemption 七、可供投资者分配的利润Profit available for owners distribution 减:应付优先股股利Less: Appropriation of preference shares dividend 提取任意盈余公积Appropriation of discretionary surplus reserve 应付普通股股利Appropriation of ordinary shares

完整英文版资产负债表、利润表及现金流量表

完整英文版资产负债表、利润表及现金流量表来 资产负债表Balance Sheet 项目ITEM 货币资金Cash 短期投资Short term investments 应收票据Notes receivable 应收股利Dividend receivable 应收利息Interest receivable 应收帐款Accounts receivable 其他应收款Other receivables 预付帐款Accounts prepaid 期货保证金Future guarantee 应收补贴款Allowance receivable 应收出口退税Export drawback receivable 存货Inventories 其中:原材料Including:Raw materials 产成品(库存商品) Finished goods 待摊费用Prepaid and deferred expenses 待处理流动资产净损失Unsettled G/L on current assets 一年内到期的长期债权投资Long-term debenture investment falling due in a yaear 其他流动资产Other current assets 流动资产合计Total current assets 长期投资:Long-term investment: 其中:长期股权投资Including long term equity investment 长期债权投资Long term securities investment *合并价差Incorporating price difference 长期投资合计Total long-term investment 固定资产原价Fixed assets-cost 减:累计折旧Less:Accumulated Dpreciation 固定资产净值Fixed assets-net value 减:固定资产减值准备Less:Impairment of fixed assets 固定资产净额Net value of fixed assets 固定资产清理Disposal of fixed assets 工程物资Project material 在建工程Construction in Progress 待处理固定资产净损失Unsettled G/L on fixed assets 固定资产合计Total tangible assets 无形资产Intangible assets 其中:土地使用权Including and use rights 递延资产(长期待摊费用)Deferred assets

完整英文版资产负债表、损益表和现金流量表

完整英文版资产负债表、利润表及现金流量表来源:冯硕的日志 资产负债表Balance Sheet 项目ITEM 货币资金Cash 短期投资Short term investments 应收票据Notes receivable 应收股利Dividend receivable 应收利息Interest receivable 应收帐款Accounts receivable 其他应收款Other receivables 预付帐款Accounts prepaid 期货保证金Future guarantee 应收补贴款Allowance receivable 应收出口退税Export drawback receivable 存货Inventories 其中:原材料Including:Raw materials 产成品(库存商品) Finished goods 待摊费用Prepaid and deferred expenses 待处理流动资产净损失Unsettled G/L on current assets 一年内到期的长期债权投资Long-term debenture investment falling due in a yaear 其他流动资产Other current assets 流动资产合计Total current assets 长期投资:Long-term investment: 其中:长期股权投资Including long term equity investment 长期债权投资Long term securities investment *合并价差Incorporating price difference 长期投资合计Total long-term investment 固定资产原价Fixed assets-cost 减:累计折旧Less:Accumulated Dpreciation 固定资产净值Fixed assets-net value 减:固定资产减值准备Less:Impairment of fixed assets 固定资产净额Net value of fixed assets 固定资产清理Disposal of fixed assets 工程物资Project material 在建工程Construction in Progress 待处理固定资产净损失Unsettled G/L on fixed assets 固定资产合计Total tangible assets 无形资产Intangible assets 其中:土地使用权Including and use rights 递延资产(长期待摊费用)Deferred assets 其中:固定资产修理Including:Fixed assets repair

中英文对照--利润表

利润表INCOME STATEMENT 项目ITEMS 产品销售收入Sales of products 其中:出口产品销售收入 Including:Export sales 减:销售折扣与折让 Less:Sales discount and allowances 产品销售净额Net sales of products 减:产品销售税金Less:Sales tax 产品销售成本 Cost of sales 其中:出口产品销售成本Including:Cost of export sales 产品销售毛利Gross profit on sales 减:销售费用Less:Selling expenses 管理费用General and administrative expenses 财务费用Financial expenses 其中:利息支出(减利息收入) Including:Interest expenses (minusinterest ihcome) 汇兑损失(减汇兑收益) Exchange losses(minus exchange gains) 产品销售利润Profit on sales 加:其他业务利润Add:profit from other operations 营业利润Operating profit 加:投资收益Add:Income on investment 加:营业外收入Add:Non-operating income 减:营业外支出Less:Non-operating expenses 加:以前年度损益调整Add:adjustment of loss and gain for previous years

损益表

损益表是指反映企业在一定会计期的经营成果及其分配情况的会计报表,是一段时间内公司经营业绩的财务记录,反映了这段时间的销售收入、销售成本、经营费用及税收状况,报表结果为公司实现的利润或形成的亏损。 中文名 损益表 外文名 income statement(美国) 外文名 profit and loss account英国 别名 利润表,损益平衡表 目录 1简介 2准则 3作用 4比较 5样式 6局限性 7指标分析 8制作 9编制方法 1简介编辑 相关表格 损益表(或利润表、损益平衡表)是用以反映公司在一定期间利润实现(或发生亏损)的财务报表。它是一张动态报表。损益表可以为报表的阅读者提供作出合理的经济决策所需要的有关资料, 可用来分析利润增减变化的原因, 公司的经营成本, 作出投资价值评价等。损益表的项目,按利润构成和分配分为两个部分。其利润构成部分先列示销售收入,然后减去销售成本得出销售利润;再减去各种费用后得出营业利润(或亏损);再加减营业外收入和支出后,即为利润(亏损)总额。利润分配部分先将利润总额减去应交所得税后得出税后利润;其下即为按分配方案提取的公积金和应付利润;如有余额,即为未分配利润。损益表中的利润分配部分如单独划出列示,则为“利润分配表”。 2准则编辑 在损益表准则起草的过程中,发现由于大部分国家和地区都没有单独的损益表准则,在一定程度上影响了会计信息的相互比较。起草损益表准则,本着既要借鉴国际惯例,又要符合中国国情这一原则,根据宏观管理的要求和各方面对企业经营成果指标的需要,才制定了统一的损益表准则。 中国《企业会计准则-损益表》分为引言、正文、附则三个部分。其中,引言部分说明了该

中英文对照财务报表常用单词

资产负债表 Balance Sheet 项目 ITEM 货币资金 Cash 短期投资 Short term investments 应收票据 Notes receivable 应收股利 Dividend receivable 应收利息 Interest receivable 应收帐款 Accounts receivable 其他应收款 Other receivables 预付帐款 Accounts prepaid 期货保证金 Future guarantee 应收补贴款 Allowance receivable 应收出口退税 Export drawback receivable 存货 Inventories 其中:原材料 Including:Raw materials 产成品(库存商品) Finished goods 待摊费用 Prepaid and deferred expenses 待处理流动资产净损失 Unsettled G/L on current assets 一年内到期的长期债权投资 Long-term debenture investment falling due in a yaear 其他流动资产 Other current assets 流动资产合计 Total current assets 长期投资: Long-term investment: 其中:长期股权投资 Including long term equity investment 长期债权投资 Long term securities investment *合并价差 Incorporating price difference 长期投资合计 Total long-term investment 固定资产原价 Fixed assets-cost 减:累计折旧 Less:Accumulated Dpreciation 固定资产净值 Fixed assets-net value 减:固定资产减值准备 Less:Impairment of fixed assets 固定资产净额 Net value of fixed assets 固定资产清理 Disposal of fixed assets 工程物资 Project material 在建工程 Construction in Progress 待处理固定资产净损失 Unsettled G/L on fixed assets 固定资产合计 Total tangible assets 无形资产 Intangible assets 其中:土地使用权 Including and use rights 递延资产(长期待摊费用)Deferred assets 其中:固定资产修理 Including:Fixed assets repair 固定资产改良支出 Improvement expenditure of fixed assets 其他长期资产 Other long term assets

财务报表(中英文版)

标准版的财务报表(中英文版) 资产负债表Balance Sheet 项目ITEM 货币资金Cash 短期投资Short term investments 应收票据Notes receivable 应收股利Dividend receivable 应收利息Interest receivable 应收帐款Accounts receivable 其他应收款Other receivables 预付帐款Accounts prepaid 期货保证金Future guarantee 应收补贴款Allowance receivable 应收出口退税Export drawback receivable 存货Inventories 其中:原材料Including:Raw materials 产成品(库存商品) Finished goods 待摊费用Prepaid and deferred expenses 待处理流动资产净损失Unsettled G/L on current assets 一年内到期的长期债权投资Long-term debenture investment falling due in a yaear 其他流动资产Other current assets 流动资产合计Total current assets 长期投资:Long-term investment: 其中:长期股权投资Including long term equity investment 长期债权投资Long term securities investment *合并价差Incorporating price difference 长期投资合计Total long-term investment 固定资产原价Fixed assets-cost 减:累计折旧Less:Accumulated Dpreciation 固定资产净值Fixed assets-net value 减:固定资产减值准备Less:Impairment of fixed assets 固定资产净额Net value of fixed assets 固定资产清理Disposal of fixed assets 工程物资Project material 在建工程Construction in Progress 待处理固定资产净损失Unsettled G/L on fixed assets 固定资产合计Total tangible assets 无形资产Intangible assets 其中:土地使用权Including and use rights 递延资产(长期待摊费用)Deferred assets 其中:固定资产修理Including:Fixed assets repair 固定资产改良支出Improvement expenditure of fixed assets

常见利润表中英文表达

利润表中英文对照版 一、主营业务收入 Revenue 减:主营业务成本 Less: Cost of Sales 主营业务税金及附加 Sales Tax 二、主营业务利润(亏损以“—”填列) Gross Profit ( - means loss) 加:其他业务收入 Add: Other operating income 减:其他业务支出 Less: Other operating expense 减:营业费用 Selling & Distribution expense 管理费用 G&A expense 财务费用 Finance expense 三、营业利润(亏损以“—”填列) Profit from operation ( - means loss) 加:投资收益(亏损以“—”填列) Add: Investment income 补贴收入 Subsidy Income 营业外收入 Non-operating income 减:营业外支出 Less: Non-operating expense 四、利润总额(亏损总额以“—”填列) Profit before Tax 减:所得税 Less: Income tax 少数股东损益 Minority interest 加:未确认投资损失 Add: Unrealised investment losses 五、净利润(净亏损以“—”填列) Net profit ( - means loss) 加:年初未分配利润 Add: Retained profits

其他转入 Other transfer-in 六、可供分配的利润 Profit available for distribution( - means loss) 减:提取法定盈余公积 Less: Appropriation of statutory surplus reserves 提取法定公益金 Appropriation of statutory welfare fund 提取职工奖励及福利基金 Appropriation of staff incentive and welfare fund 提取储备基金 Appropriation of reserve fund 提取企业发展基金 Appropriation of enterprise expansion fund 利润归还投资 Capital redemption 七、可供投资者分配的利润 Profit available for owners distribution 减:应付优先股股利 Less: Appropriation of preference shares dividend 提取任意盈余公积 Appropriation of discretionary surplus reserve 应付普通股股利 Appropriation of ordinary shares dividend 转作资本(或股本)的普通股股利 Transfer from ordinary shares dividend to paid in capital 八、未分配利润 Retained profit after appropriation 补充资料: Supplementary Information: 1. 出售、处置部门或被投资单位收益Gains on disposal of operating divisions or investments 2. 自然灾害发生损失 Losses from natural disaster 3. 会计政策变更增加(或减少)利润总额 Increase (decrease) in profit due to changes in accounting policies 4. 会计估计变更增加(或减少)利润总额 Increase (decrease) in profit due to changes in accounting estimates 5. 债务重组损失 Losses from debt restructuring

损益表分类

损益表分类 I.店内损益表分类 A.收入 1.销售净额-包括所有现金、现金抵用劵 2.折扣/优劵 3.销售毛额=销售净额-折扣/优惠劵 B.支出、 1.食物成本-所有作销售食品的原材料或向第三方生产商采购的费用。 2.食物包装材料-所有外卖包装器皿、外卖食具及塑料袋等费用。 3.毛利=销售毛额-食物成本-食物包装材料 4.场地成本 a.租金-餐厅向业主所缴交的租金(保底或百分比租金)。 b.折旧-根据开店的资本开支来每月摊分。 c.商场空调费/推广费/杂费-商场根据店铺面积向店铺每月收取 的定额收费。 5.劳工成本 a.工资(服务员)-所有服务员、厨房员工的工资。 b.工资(管理人员)-店经理或以上管理人员的工资。 c.宿舍-服务员宿舍租金、电费、水费及管理费等。 d.伙食费-公司提供的员工餐材料及外煮食人员的工资,或餐费津贴。 e.其他劳工成本-包括所有附带福利、保险金及养老福利等。 6.水电-商场向店铺收取实报实销的水费、电费、煤气费或排污费等。 7.电讯-包括电话费、宽带费。 C.清洁耗材-所有清洁器皿、清洁餐厅及洗手消毒用品等耗材的费用。 D.营运耗材-除了清洁物资的店内消耗性费用,如收银机打印纸。 E.现金差额-所收现金与收银系统纪录的差额。 F.保险金-所有非员工福利的保险金,例如第三者责任保险及火险等。 G.非盈利税项-所有餐厅营运所产生的非盈利税项,包括增值税及营业税等。 H.保养维修-所有设备、场地及空调维修等费用。 I.市场费用-所有促销、店内宣传资料、餐牌、季节性装饰的设计及制作费 用。

总部 I.行政开支-银行费用及其他行行政费用。 II.出差及招待开支-出差路费、住宿费、餐费、招待客人费用。III.汽车-汽车相关费用。

利润表中英文对照版

会计从业、初级、中级题库下载:https://www.360docs.net/doc/8d15247101.html,/ztalldown/?wenku 利润表中英文对照版 一、主营业务收入 Revenue 减:主营业务成本 Less: Cost of Sales 主营业务税金及附加 Sales Tax 二、主营业务利润(亏损以“—”填列) Gross Profit ( - means loss) 加:其他业务收入 Add: Other operating income 减:其他业务支出 Less: Other operating expense 减:营业费用 Selling & Distribution expense 管理费用 G&A expense 财务费用 Finance expense 三、营业利润(亏损以“—”填列) Profit from operation ( - means loss) 加:投资收益(亏损以“—”填列) Add: Investment income 补贴收入 Subsidy Income 营业外收入 Non-operating income 减:营业外支出 Less: Non-operating expense 四、利润总额(亏损总额以“—”填列) Profit before Tax 减:所得税 Less: Income tax 少数股东损益 Minority interest

会计从业、初级、中级题库下载:https://www.360docs.net/doc/8d15247101.html,/ztalldown/?wenku 加:未确认投资损失 Add: Unrealised investment losses 五、净利润(净亏损以“—”填列) Net profit ( - means loss) 加:年初未分配利润 Add: Retained profits 其他转入 Other transfer-in 六、可供分配的利润 Profit available for distribution( - means loss) 减:提取法定盈余公积 Less: Appropriation of statutory surplus reserves 提取法定公益金 Appropriation of statutory welfare fund 提取职工奖励及福利基金 Appropriation of staff incentive and welfare fund 提取储备基金 Appropriation of reserve fund 提取企业发展基金 Appropriation of enterprise expansion fund 利润归还投资 Capital redemption 七、可供投资者分配的利润 Profit available for owners distribution 减:应付优先股股利 Less: Appropriation of preference shares dividend 提取任意盈余公积 Appropriation of discretionary surplus reserve 应付普通股股利 Appropriation of ordinary shares dividend 转作资本(或股本)的普通股股利 Transfer from ordinary shares dividend to paid in capital 八、未分配利润 Retained profit after appropriation 补充资料: Supplementary Information: 1. 出售、处置部门或被投资单位收益 Gains on disposal of operating divisions or investments 2. 自然灾害发生损失 Losses from natural disaster