Australian taxation law notes 澳大利亚税法概要

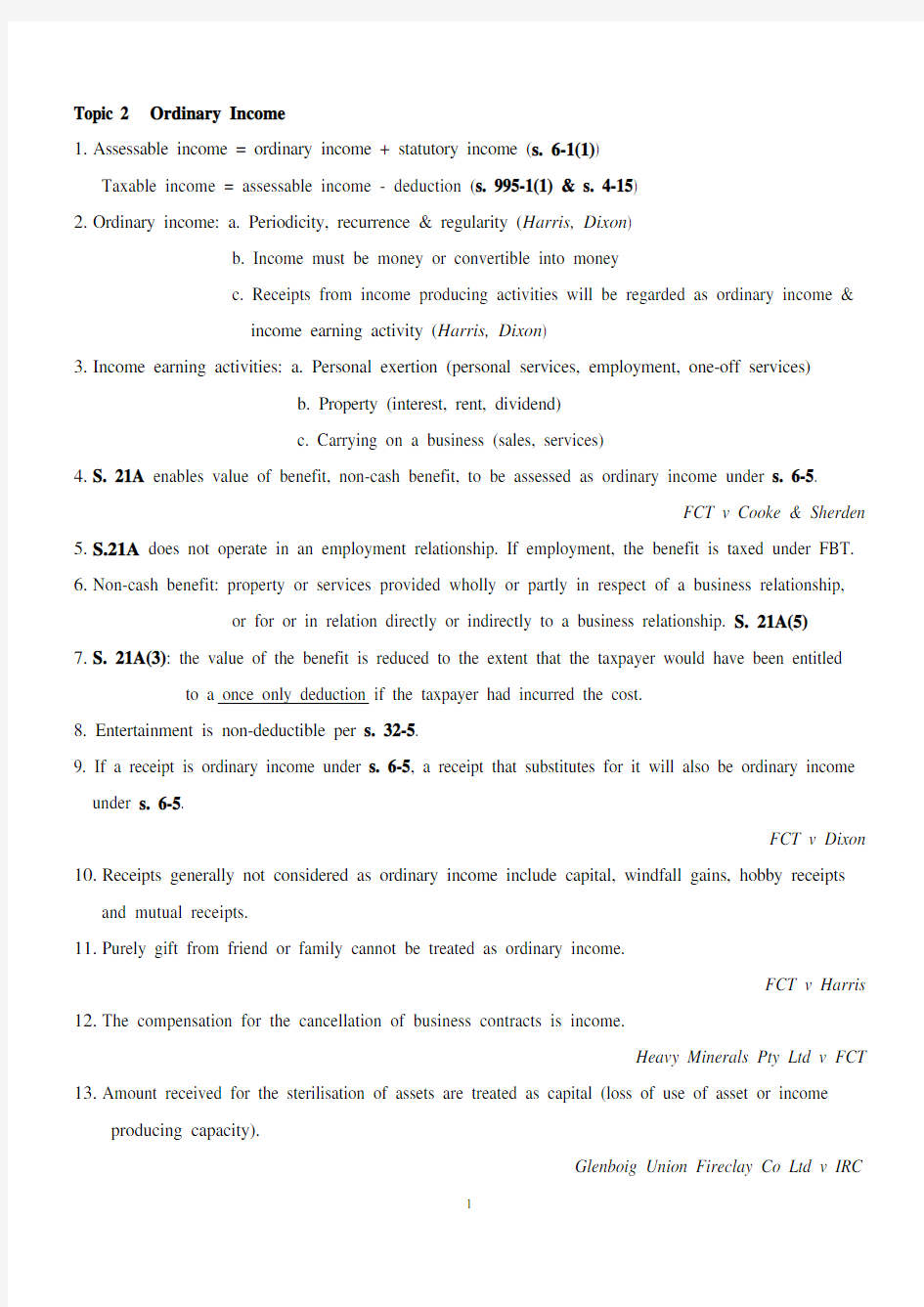

Topic 2 Ordinary Income

1.Assessable income = ordinary income + statutory income (s. 6-1(1))

Taxable income = assessable income - deduction (s. 995-1(1) & s. 4-15)

2.Ordinary income: a. Periodicity, recurrence & regularity (Harris, Dixon)

b. Income must be money or convertible into money

c. Receipts from income producing activities will be regarded as ordinary income &

income earning activity (Harris, Dixon)

3.Income earning activities: a. Personal exertion (personal services, employment, one-off services)

b. Property (interest, rent, dividend)

c. Carrying on a business (sales, services)

4.S. 21A enables value of benefit, non-cash benefit, to be assessed as ordinary income under s. 6-

5.

FCT v Cooke & Sherden

5.S.21A does not operate in an employment relationship. If employment, the benefit is taxed under FBT.

6.Non-cash benefit: property or services provided wholly or partly in respect of a business relationship,

or for or in relation directly or indirectly to a business relationship. S. 21A(5)

7.S. 21A(3): the value of the benefit is reduced to the extent that the taxpayer would have been entitled

to a once only deduction if the taxpayer had incurred the cost.

8. Entertainment is non-deductible per s. 32-5.

9. If a receipt is ordinary income under s. 6-5, a receipt that substitutes for it will also be ordinary income under s. 6-5.

FCT v Dixon 10.Receipts generally not considered as ordinary income include capital, windfall gains, hobby receipts

and mutual receipts.

11.Purely gift from friend or family cannot be treated as ordinary income.

FCT v Harris 12.The compensation for the cancellation of business contracts is income.

Heavy Minerals Pty Ltd v FCT 13.Amount received for the sterilisation of assets are treated as capital (loss of use of asset or income

producing capacity).

Glenboig Union Fireclay Co Ltd v IRC

14. Payments received for entering into restrictive agreements are capital.

Dickenson v FCT 15. Compensation for loss of trading stock is considered as income.

CIR v Newcastle Breweries Ltd 16. Sales of knowledge or ‘know-how’ are income.

Rolls-Royce Ltd v Jeffrey 17.Sale or assignment of income streams should be treated as income, and the lump sum is assesable

under s. 25(1).

Myer Emporium 18.Undissected lump sum, where lump sum amounts comprising both income and capital, but without

dissection into their actual components, should be treated as capital.

Mclaurin v FCT

19. Lottery prize are not income in the Australian jurisdiction.

20. Gambling wins will only constitute deduction and assessable income, if they may be seen as proceeds

of a business.

Trautwein v FCT

21. Receipts form gambling wins are not assessable. (Martin v FCT)

22.No liability to tax arises where a person participates casually in a competition and wins a prize.

However, a professional quiz player regular appearances on quiz programs the prizes may constitute assessable income.

Case T14 23.Receipts or proceeds form hobbies, as distinguished from business, are deemed not to be assessable

income. Also, expenses and losses from hobbies are not deductibel.

https://www.360docs.net/doc/6a9714773.html,anizations have no identity separate from their members, thus subscriptions and other

contributions form members cannot be treated as income, they are mutual in character.

The Bohemians Club v Acting FCT 25. Income from illegal activities are assessable.

Partridge v Mallandaine 26. Profits arising from ultra vires actions of company directors may be assessable of the company.

England v Webb

Topic 3 Derivation of Income

1.S 6-5(2) & (3): assessable income include ordinary income derived during the income year.

2.The cash basis: used mostly by individuals, eg salary or wage earners

The accruals basis: generally used in business

3.Cash basis: income is derived when the cash is received.

Brent v FCT Accruals basis: the income is derived when it has been earned, when an invoice has been issued.

J Rowe & Son v FCT 4. Large chartered accounting firm should use accruals basis, because the income is not personal services income, it is the result of many accountants.

Henderson v FCT 5. The income derived by a solicitor in sole practice with one secretary should be treated as personal

services income and cash basis appropriate.

FCT v Firstenberg 6.Services can be provided by many people - Accrual

Services provided by one person - Cash

Selling shoes by one or many people - trading business - Accrual

Income from rental property - Cash

7.For a business selling goods or supplying services, amounts received in advance are not regarded as

income.

Arthur Murray v FCT 8.S. 6-5(4): the case where the taxpayer, though he has not received the money itself, has had the benefit

of it, or of something which is substantially equivalent to it. (cash basis only)

9. Brent v FCT: Wife of the Great in not in business instead providing personal services - Cash basis

S. 6-5(4) did not apply, and only the money actually received was derived.

10. Asking for a cash payment to be delayed is not dealing with the income. (cash basis only)

Brent v FCT

Topic 4 Statutory Income and Exempt Income

1.Dividends paid by a company to a shareholder are included in the shareholder’s assessable income

under s. 44(1).

2.Tax paid on the profits from which a dividend was paid and passed onto the shareholder is also

assessable under s. 207-20(1), which is called ‘franking’.

从税后利润付股利给股东,这部分利润所含的已交公司所得税称为franking credit。股东应申报(股利+franking credit)为总股利,按照自己的税率,再减去franking credit,就是这部分收入应交的个人所得税。

3.S. 15-2(1): includes the value to the taxpayer of allowances, gratuities, compensations, benefits, bonuses and premiums provided, directly or indirectly, with respect to employment or services.

4.S. 15-2(2): does not have to be in the form of money.

5.S. 15-2(3)(d): if the allowance etc is ordinary income under s. 6-5, then s. 15-2 will not operate.

6. S. 6-25(2): cannot assess income twice.

7. S. 15-3: payments only made to induce a resumption of work are included in assessable income.

8. S. 15-10: your assessable income includes a bounty or subsidy that is paid a government to assist in the carrying on of a business, where the amount is not ordinary income assessable under s. 6-5.

9.S. 15-15: profits arising form the carrying on or carrying out of a profit-making undertaking or plan is included in assessable income, except where the profit is ordinary income assessable under s. 6-5.

10. Due to capital gain, s. 15-15 often not apply, there just in case.

11. Ordinary meaning of ‘Royalties’: 为行使某种权利而支付的费用,并且有数量上的规定。

McCauley v FCT 12. S. 15-20: your assessable income includes an amount that you received as or by way of royalty within

the ordinary meaning of ‘royalty’ and is not ordinary income under s. 6-5(1).

13.S. 15-30: any amount you received by way of insurance or indemnity for the loss of an amount is

included in assessable income, and the amount received is not ordinary income assessable under s.

6-5.

14. S. 15-35: If a taxpayer overpays their tax, interest paid on that tax by the ATO is assessable.

15. S. 15-70: reimbursement for car expenses on a cents per kilometer basis will be assessable.

This is different from a ‘car allowance’ which is ordinary income under s. 6-5(1).

Here, the employee is given extra money from employer to pay for car expenses.

16. S. 83-10: unused annual leave paid out as a lump sum on termination of employment is assessable.

17. S. 83-70: long service leave paid out is assessable.

18. S. 23L(1): income derived via a fringe benefit is not assessable as ordinary income.

19. S. 23L(2): non-cash business benefits within the meaning of s. 21A that are valued at less than $300 is

exempt.

Topic 5 Residence and Source

1.S. 6-5(2): if you are an Australian Resident, your assessable income includes the ordinary income you

derived from all sources.

2.S. 6-5(3): if you are a foreign resident, your assessable income includes ordinary income derived

directly or indirectly from all Australian sources, and other ordinary income that a provision

Includes.

4.Dictionary definition of ‘Reside’: To dwell permanently or for a considerable time, to have one’s

settled or usual abode, to live in or at a particular place. Residence of individual

5. Three tests: a. a person who resides in Australia. (Common Law Test)

b. a person whose domicile is Australia, unless the Commissioner is satisfied that they

have a permanent place of abode outside Australia. (Domicile Test)

c. a person who satisfies the 183 day rule.

6. From Levene v IRC: a. A person may leave their residence from time to time for business or pleasure.

Pechey v FCT

b. A person who visit another country without setting up an establishment is not a

resident there.

c. A person may reside in more than one place. (Gregory v DFCT)

7. Domicile is a legal concept and refers to the legal relationship a person has with a state.

Henderson v Henderson 8. A place of abode is a man’s residence, where he lives with his family and sleeps at night.

R v Hammond

9. Permanent does not equal forever, less than forever, but more than just holiday.

10. Permanent means more than simply temporary or transitory, but less than everlasting

FCT v Applegate 11.Under Domicile Test, a person will be a resident of Australia, if his domicile is Australia, unless his

permanent place of abode is outside Australia.

12. Permanent place of abode outside Australia:

a. Intended and actual length of stay, greater than 2 years suggests non-residency.

b. Establishment of a home outside Australia.

c. Durability of association with Australia.

13. 183 day rule: will be a resident for tax if have a presence in Australia for more than half of the

income year, either continuously or intermittently. (mainly applicable to people coming

into Australia)

14.Second limb of 183 day rule: a person will not be a resident of Australia Under this test, if the

Commissioner is satisfied that the taxpayer has a permanent place of abode

outside Australia.

Residence of companies

15. Three tests in para (b) of the definition of resident in s. 6(1): (only one need to be satisfied)

a. Incorporation test

b. Central management and control test

c. Controlling shareholder test

16: Incorporation test: a company is an Australian resident for tax, if it is incorporated in Australia. 17.Central management and control test: a company is an Australian resident for tax, if it carries on

business in Australia, and has its central management and

control in Australia.

Malayan Shipping v FCT 18.The central management and control of a company will usually be where the directors exercise their

powers of management.

De Beers Consolidated Mines v Home 19.If there is more than one place of management, the central management and control will be where the

‘superior or directing authority’ of the company is located.

Koitaki Para Rubber Estates Ltd v FCT 20.Controlling shareholder test: a company will be a resident of Australia for tax, if it carries on

Business (trading activity only) in Australia, and has its voting power

controlled by shareholders who residents of Australia.

Source of income

21.Payment for services - generally where the work was performed, but in Mitchum v FCT where the

place of signing a contract for services was decisive.

22.Dividends - the source is the same as the source of the company’s profits.

Nathan and Esquire Norminees 23.Interest - generally where the agreement to pay the interest is made.

Studebaker v C of T 24.Royalties - the source is usually where the persons with the know-how or who supply the services

reside.

FCT v United Aircraft Corporation 25.Business or trading income - the place where the agreements are made and the transactions entered

into.

Tariff Reinsurances v DCT

Topic 6 Capital Gains Tax (CGT)

1. The net capital gain is assessable under s. 102-5(1).

2. Meaning of CGT asset S. 108-5(2): a. Part of, or an interest in, any kind of property or legal right.

b. Goodwill

c. An interest in an asset of a partnership.

d. Partnership interests not covered by the abov

e.

3. Exemptions: a. S. 118-5: cars & motor cycles; decorations for brave conduct(奖章), unless bought.

b. S. 118-12: asset used to produce exempt income.

c. S. 118-25: trading stock (never capital, it is asset)

d. S. 104-10(5)(a): assets acquired before September 1985.

e. S. 118-24: depreciable assets with 100% taxable use.

4.Three category of CGT assets: a. CGT assets

b. Collectables

c. Personal use assets

5. Collectable s. 108-10(2): a. Specific items listed (jewelry, art work, first day cover coins)

b. Kept mainly for personal use and enjoyment

c. Exempt from GST if acquired for $500 or less under s. 118-10(1)

6.Personal use assets s. 108-20(2): a. A CGT asset, except a collectable, that is mainly for personal use

and enjoyment.

b. Does not include land and buildings or units (s. 108-20(3))

c. Exempt if acquired for $10,000 or less under s. 118-10(3)

7. Capital loss from personal use assets are disregarded under s. 108-20(1).

8. S. 108-10(4): Capital loss from collectables can only be offset against gains from other collectables.

9. S108-15(2): Sets of collectables are taken to be a single collectable.

10. CGT event A1- disposal of a CGT asset: s. 104-5

A. The event occurs if you disposal of a CGT asset (s. 104-10(1))

B. Disposal is a change of beneficial ownership (s. 104-10(2))

C. Capital gain = capital proceeds - cost base (s. 104-5 & s. 104-10(4))

D. Capital loss = reduced cost base - capital proceeds (s. 104-5 & s. 104-10(4))

11.Timing of event A1: CGT event A1 occurs when you enter the contract for disposal, or;

If there is no contract, when the change of ownership occurs.

S. 104-5, S. 104-10(3) & S. 109-5(2) 12.Capital proceeds s. 116-20(1): the money received or receivable, and the market value you have

received or entitled to receive.

13.Cost base s. 110-25: a. The amount paid (s. 110-25(2))

b. Incidental cost of disposal (s. 110-25(3))

c. Capital expenditure to upgrade the asset that relates to installing or moving

asset (s. 110-25(5))

14. Incidental cost: a. Cost of surveyor, value, broker (s. 110-35(2))

b. Cost of transfer (s. 110-35(3))

c. Stamp duty印花税or similar duty (s. 110-35(4))

d. Cost of advertising for selling and buying (s. 110-35(5))

e. Cost of obtaining a valuation (s. 110- 35(6))

f. Search fees (s. 110-35(7))

15.Indexation cost base (s. 960-275(2)) = Index number at quarter ending 30 Sept 1999 (always 68.7)

Index number at quarter of purchase (check index table)

Table of index numbers: Taxation Law, p. 327 16.Discounting: a. Available only to individuals, trusts and superannuation funds. Not available to

companies (s. 115-10)

b. Available for assets purchased after 21/9/1999 and held for more than 12 months (s.

115-15, s. 115-25)

c. The net capital gain is reduced by 50% for individuals and trusts (s. 115-100(a)) Summary

17. If disposed of asset on or before 21/9/99:

A. Held asset > 12 months: indexation s. 114-1 & s. 114-10(1)

B. Held asset ≤ 12 months: indexation not available s. 114-10(1)

C. Discounting not exist before 21/9/99

18. If disposed of asset after 21/9/99 and asset was acquired on or before 21/9/99:

A. Held asset < 12 months: no indexation s. 114-10(1), no discounting s. 115-25(1)

B. Held asset ≥ 12 months: can choose indexation s. S.114-1 & s. 114-10(1), or discounting

s. 115-15 & s. 115-25(1)

C. Company cannot discount at all (s.115-10)

19. If asset was disposed of and acquired after 21/9/99:

A. Held asset >12 months: discount available s. 115-15 & s. 115-25(1)

B. Held asset ≤ 12 months: no discount s. 115-25(1)

C. Indexation not available at all s. 114-1

D. Company cannot discount at all (s.115-10)

20.Often discounting will be better, but not when there are large carry forward losses, and company can

only index (if available)

21.Steps in calculation: a. CGT asset? S. 108-5, disposal of asset event A1

b. Exemptions?

c. Type of CGT asset?

d. If you have a gain, consider the concessions: Indexation s. 114-1 & s. 114-10

Discounting s. 115-5,-10,-15,-20

c. Calculate the gain/loss

Topic 7 Fringe Benefits Tax (FBT)

1.FBT is only relevant for non-cash employment benefits. Non-cash business benefits are dealt with

under s. 21A and still assessed under s. 6-5(1).

Step 1 - a fringe benefit?

2.Employment relationship: for a benefit to be a fringe benefit, it must be provided in respect of the

employment of the employee, not because of other relationship. (most

important, cannot employ yourself)

3. Benefit: includes real or personal property and the rights to use such property.

4. Provided in FBT year: in the period 1 April to 31 March 2014.

5. Provider of the benefit: employer, associate or arranger.

6. Recipient: employee; current, past, or future employee; associate of the employee.

Step 2 - a car benefit?

7.S. 7(1)(a): A. provided due to employment;

B. held by an employer, associate or third party;

C. applied for private use;

D. available for private use

8. Definition of a car: s. 136(1) FBTAA86 & s. 995-1(1) ITAA97

A. Motor vehicle (except motorcycle or similar)

B. Designed to carry less than 1 tonne and less than 9 passengers

9. Applied for private use: s. 7(2) & (3)

A. Private use can be deemed if the car is available for private use.

B. If the car is garage at or near a place of residence of the employee, it is considered

available for private use (s. 7(2)(b)), and

C. Use that is not in the course of producing assessable income of the employer

(s. 7(3)(c)(i) & s. 136(1))

10.Exempt car benefits: a. Taxis, panel vans, utes or other motor vehicles where the private use is of a

minor, infrequent and irregular (s. 8(2))

b. Unregistered cars that are used mainly in connection with the business of the

Employer (s. 8(3))

Step 3 - calculating taxable value

11. Statutory formula s. 9(1): ABC - E

D

A = Base value of the car (cost price s. 9(2)(a)(i))

The sum of Expenditure incurred (exclude registration cost and cost of transfer), and

Additional expenditure incurred in relation to fitting non-business accessories.

B = Statutory fraction

C = Number of days benefit provided in a year

D = Number of days in tax year

E = Recipient’s contribution to the benefit

12. If the car is leased: base value = leased car value (s. 9(2)(a)(ii))

13. Leased car value s. 136(1): a. The cost price to the lessor if the person began leasing the car at the

same time as the lessor bought it.

b. The amount that the person could reasonably be expected to pay to

purchase the car from the owner under an arm’s length transaction. 14.Cars owned by employer: the base value is reduced to 2/3 of the original value in the year after the 4th

anniversary of purchase (s. 9(2)(a)(i))

15. Cars leased by employer: the base value is reduced to 2/3 of the original value in the year after the 4th

anniversary of purchase (s. 9(2)(a)(ii))

16.Recipient’s contribution s. 9(2)(e): this come in the form of the employee paying for some petrol,

repairs, etc. or just making a cash contribution.

17. Operating cost formula s. 10(2): C × (100% - BP) - R

C = total of all operating costs during the FBT year

BP = business use percentage

R = recipient’s contribution

18.Car is owned, operating costs are:

A. Car expenses eg. petrol, oil, servicing paid for s. 10(3)(a)(i)

B. Registration and insurance s. 10(3)(a)(ii)

C. Deemed depreciation s. 10(3)(a)(iii)(A)

D. Deemed interest s. 10(3)(a)(iii)(B)

19.Car is leased, operating costs are:

A. Lease fees s. 10(3)(a)(v)(A)

B. Car expenses (petrol, oil, servicing, repair paid for) s. 10(3)(a)(i)

C. Registration and insurance s. 10(3)(a)(ii)

20. Recipient’s contribution: same as the definition in the statutory formula, but section is different here

(S. 10(2) & s. 10(3)(c))

21 Deemed depreciation = ABC s. 11(1A), 11(1), 11(1AA) & s. 12

D only relevant if the car is owned

A = cost price or depreciated value

B = currently 25% depreciation rate (subsection 1AA)

C = number of days owned in the FBT year

D = number of days in the year of tax

22. Deemed interest = ABC s. 11(1B) & s. 11(2)

D only relevant if the car is owned

A = cost price or depreciated value

B = statutory interest rate (6.45% for 2013/14)

C = No. of days owned in the FBT year

D = Number of days in the year of tax

23. Calculate both statutory and operating, choose the lowest one.

24. Employer can elect between statutory and operating under s. 10(1).

25. If elect operating cost and the statutory provide lower FBT, s. 10(5) provides that the election be

disregarded.

Topic 8 General Deductions

1. S. 4-15(1): Taxable income = Assessable income - Allowable deductions

2. You can deduct any loss or outgoing under s. 8-1(1): (positive limbs)

A. It is incurred in gaining or producing assessable income, or

(a vailable to all taxpayers, but generally applied to employees)

B. It is incurred in carrying on a business for the purpose of gaining or producing

your assessable income.

(only applicable to business taxpayer)

3. You cannot deduct a loss or outgoing under s. 8-1(2): (negative limbs)

A. The loss or outgoing is capital in nature s. 8-1(2)(a)

B. The loss or outgoing is private or domestic in nature s. 8-1(2)(b)

C. The loss or outgoing was incurred whilst gaining exempt income

*Any one of above satisfied, you cannot be deducted

4. Outgoing = expenditure paid or liability incurred

Loss = same as outgoing

Amalgamated Zinc v FCT 5.Employees were lobbed whilst going to the bank to deposit the day’s taking, the loss by robbery was

incurred in carrying on a business for producing assessable income, it’s deductible (存钱被抢).

Charles Moore & Co v FCT First Positive Limb

6. Expenditure may be deductible, if it will reduce future expenses (裁员所付的赔偿金).

W Nevill & Co 7. Expenditure may relate to income from preceding or future years.

AGC Ltd v FCT Second Positive Limb

8. Costs incurred before a business starts are not usually deductible.

Softwood Pulp & Paper 9. Costs in establishing a new part of a business are not deductible.

Griffin Coal Mining

10. Expenditure after cessation of a business may not be deductible.

Amalgamated Zinc v FCT

11.If the loss could be related back to an earlier income activity, the expenditure may be deductible after

a business has ceased.(旧公司被收购后,旧公司在旧业务中导致的亏损,新公司可以申请抵税)

AGC Ltd v FCT 12.Interest payment that incurred on a loan after the sale of the business in respect of which the loan was

taken out as a deduction is deductible.

(公司停业后,其停业之前用作收购业务的贷款所需支付的利息可以抵税)

FCT v Brown 13.Provided the occasion for the loss or outgoing is to be found in the business operations directed to

gaining or producing assessable income, the loss will be deductible unless it is of a capital nature. (公司在停业之前因业务问题给客户造成的损失而导致的法律纠纷,其法律纠纷所付的钱可以抵税)

Placer Pacific v FCT Judicial Test

14. Incidental and relevant test: The occasion of the loss or outgoing should be found in whatever is

productive of the assessable income or, if none be produced, would be expected to produce

assessable income.

(该结论在Charles Moore中应用)

Ronpibon Tin 15. Essential character test: two taxpayers’ claims for travel costs from home to work were denied.

(上班的车费是derive income 的先决条件,并没有实际导致derive income,不能抵税)

Lunney v FCT 16.S. 25-100: to allow a deduction to an individual taxpayer from the 2001-2002 year for direct travel

between two places of work.

17.S. 25-100(3): a deduction is not allowed under this section if one of the work places is also the

taxpayer’s residence.

Apportionment

18.Apportionment allows a deduction for the expenditure that is not private or capital or not used to

produce exempt income.

我国个人所得税概况

[摘要] 本文介绍了我国个人所得税目前的状况,对当前我国个人所得税制度存在的弊端以及在征税过程中遇到的问题,并根据我国的实际情况提出了对个人所得税制度的改革,政府应该加强对个人所得税征收的力度。个人所得税对我国现在以及未来财政收入有着巨大的影响,现在个人所得税占国家税收收入的比例过低,所以在未来几年我国还要根据社会主义市场经济不断的发展,对个人所得税制度不断的完善,为经济持续发展和社会和谐打好基础。 [关键词] 个人所得税,纳税筹划,问题,税收

目录 一、所得税的概念及其意义 (3) 二、我国个人所得税征管制度存在的问题 (4) (一)税款使用制度欠缺影响纳税积极性 (4) (二)全国适用同一费用扣除标准不符合实际 (4) (三)税率设置存在不公平 (4) (四)所得税分类税制模式征税范围过于狭窄 (4) (五)纳税人的权利与义务不对等 (5) 三、改进我国个人所得税征管的措施 (5) (一)重塑政府在个人所得税征管中的形象 (5) (二)改革完善个人所得税制 (6) (三)加强法制建设和个人所得税法宣传,创造良好的依法治税环境 (7) (四)建立有效的个人收入监管机制 (8) (五)完善初次分配和税收征管配套政策 (8) 一、个人所得税的概念及其意义 个人所得税,就是对个人获得的各种应税所得征收的一种税。它于1799年始

创于英国,至今已有200年的历史。由于个人所得税在世界税收史上具有税基广、弹性大、调节收入分配和促进经济增长等诸多方面的优点,它正在世界各国逐步得到广泛的推广,不仅成为许多国家财政收入的主要来源。据统计,目前一些经济发达国家的个人所得税收入占当地政府财政收入的比重平均可达45%左右,且仍处于上升趋势。在我国,个人所得税也已成为税制中的重要税种之一。1993年1月31日,八届人大常委会四次会议通过的《中华人民共和国个人所得税法》,标志着我国个人所得税的发展开始步入正轨。 个人所得税能缩小个人收入差距,缓解社会分配不公的矛盾,合理分配社会资源。对建设社会主义社会和谐,国民经济的健康发展有着重要的影响。 我国的居民收入差距越来越大。它可能引起社会不稳定。事实上,收入的集中化与不平等正开始妨碍中国的社会和经济发展。在这个意义上,壮大个人所得税就不仅是长远需要,而且是一种迫切需要。我国以间接税为主体的税制本身不具备调节经济的功能,这与我国特有的经济结构有关。私人经济规模尽管已经不小,但质量不高;国有经济因产权原因,并非完全市场微观主体,它们都没有对调控政策作出迅速灵敏反应的能力。税制应及时作出制度安排发挥个人所得税调节功能。 在扣除项目和标准上。在分类课征的模式下,我国个人所得税的扣除项目只有计税工资,一定比例扣除等方式,是全国统一的标准,无法反映纳税人的真正纳税能力和负担水平。而国外个人所得税,比如美国的税制是以家庭和个人相结合的纳税单位设计,税务部门综合考虑家庭的收入状况,费用状况,在医疗,教育,养老等方面都有相应的扣除规定。 社会较多财富的人,应为个人所得税的主力纳税人。而我国的现状是:处于中间的、收入来源主要依靠工资薪金的阶层缴纳的个人所得税占全部个人所得税收入的46.4%;应作为个人所得税缴纳主要群体的上层阶层(包括在改革开放中发家致富的民营老板、歌星、影星、球星及建筑承包商等名副其实的富人群体),缴纳的个人所得税只占个人所得税收入总额的5%左右。个人所得税征管首要问题是明确纳税人的收入,当前什么是一个纳税人的真正全部收入是一件难事,至少有下列行为税务机关很难控制。一是收入渠道多元化。一个纳税人同一纳税期内取得哪些应税收入,在银行里没有一个统一的账号,银行方面不清楚,税务方面更不清楚。二是公民收入以现金取得较多(劳动法规定工资薪金按月以现金支付),与银行的个人账号不发生直接联系,收入难于控制。三是不合法收入往往不直接经银行发生。正因为有上述情况,工薪收入者就成了个人所得税的主要支撑。 二、我国个人所得税征管制度存在的问题 (一)税款使用制度欠缺影响纳税积极性

澳大利亚工资分配制度

澳大利亚工资分配制度 文/马文堂 收入分配基本情况 20世纪90年代前,澳大利亚工资分配标准主要是通过联邦或各州产业关系委员会或劳资法庭裁定的大约3200个工资率确定。 1996年澳实施了《工作场所关系法》,对裁定工资率体系进行大幅度改革,除保留少数裁定工资率作为确定工资的标准外,绝大多数其他劳动条件主要通过企业集体谈判或雇员单独同雇主直接 协商来确定。现在澳企业工资由裁定工资率确定的占24.1%,由集体谈判确定的占35.3%,由个人劳动合同确定的占40.6%。总体发展趋势是,裁定工资率的总体作用在下降,但在餐饮业仍比较受欢迎,采用率高达65%;集体谈判和个人协商方式的作用在上升,前者主要在公共部门、大企业和全日制工作中流行,采用率分别达80%、79%和37%;而后者则受到私营部门、小企业及专业和管理人员的青睐,采用率分别达到50%、68%和75%。 从管理与非管理职业角度看,随着最低工资标准的实行和不断提高,非管理人员的工资收入标准在不断提高,管理与非管理人员之间的工资收入差距在逐渐缩小;从性别角度看,女性雇员工资收入

大大低于男性,约为男性的66%左右,而且这种差距在过去20年基本上没有改变;从行业角度看,雇员工资收入最高的前三位依次是采矿业、金融保险业和房地产业,工资收入最低的是零售业和旅馆餐饮业。 企业的工资分配 1、工资分配模式 大中型企业非管理雇员的工资目前主要是通过企业集体谈判或个人同雇主单独协商的方式来确定。雇员收入分为货币报酬和非货币报酬,货币报酬又分为直接工资和间接收入。直接工资收入主要包括基本工资、奖金和生活费;间接工资收入包括法律规定的带薪休假和雇主提供的奖励计划,如利润分享计划等。非货币报酬,又称为“工资包”,主要是指各种激励计划,包括个人奖金、小组奖金、目标奖金、收益分享、利润分享、雇员持股等形式。这种非货币报酬主要是针对企业高级技术人员和非一般行政管理人员的,职务越高,非货币报酬越多。 2、雇员增资机制 20世纪50-60年代,澳大利亚经济快速增长,政府对工资

生产经营个人所得税计算实例

培训资料: 个人所得税申报表(A表)填写案例讲解 案例一: 甲为一家五金店(个体工商户)A的业主,该个体工商户生产经营所得个人所得税征收方式是查账征收,2017年1月至4月A收入总额100万元,累计发生成本费用80万元,可弥补以前年度亏损10万元,1月至3月累计已预缴生产经营所得个人所得税1万元。甲有听力残疾,有残疾人联合会出具的残疾人证,并已按相关文件要求办理了残疾、孤老人员和烈属劳动所得定额减征个人所得税备案手续。甲该如何申报生产经营所得个人所得税? 解答: 收入总额=1000000(元) 成本费用=800000(元) 利润总额=1000000-800000=200000(元) 弥补以前年度亏损=100000(元) 投资者减除费用=3500×4=14000(元) 应纳税所得额=200000-100000-14000=86000(元) 税率30% 速算扣除数9750 应纳税额=86000×30%-9750=16050(元) 减免税额=375×4=1500(元) 已预缴税额=10000(元) 应补(退)税额=16050-1500-10000=4550(元)

案例二: 甲为一家个人独资企业A的投资人,该个人独资企业生产经营所得个人所得税征收方式是查账征收,2017年1月至2月A收入总额40万元,累计发生成本费用35万元,可弥补以前年度亏损0元,1月累计已预缴生产经营所得个人所得税2000元,甲购买了符合财税〔2015〕126号规定的商业健康保险产品,每月支付保费200元。甲该如何申报生产经营所得个人所得税? 解答: 收入总额=400000(元) 成本费用=350000(元) 利润总额=400000-350000=50000(元) 投资者减除费用=3500×2+200×2=7400(元) 应纳税所得额=50000-7400=42600(元) 税率20% 速算扣除数3750 应纳税额=42600×20%-3750=4770(元) 已预缴税额=2000(元) 应补(退)税额=4770-2000=2770(元)

碳相关英语术语

商讨discuss 碳市场carbon market 碳贸易carbon trade 碳市场carbon market 市场规模market size 京都议定书Kyoto Protocol 碳资产carbon asset 联合国气候框架公约United Nations Framework Convention on Climate Change 签署国signatory 节能减排战略energy saving and emission reducing strategy 联合国环境与发展会议United Nations Conference on environment and development 配额型交易(Allowance-based transactions)欧盟的欧盟排放权交易制(European Union Greenhouse Gas Emission Trading Scheme,EU ETS)英国的英国排放权交易制(UK Emissions Trading Group, ETG) 欧盟和英国的交易所是国际性的 美国的芝加哥气候交易所(Chicago Climate Exchange,CCX) 澳大利亚的澳大利亚国家信托(National Trust of Australia,NSW) 温室气体greenhouse gas

减排emission reducing 国际公法international public law 交易transaction 二氧化碳carbon dioxide emission 前景future prospect 爆炸式增长explosive growth/ rocketly growth 成交额the volume of business 欧元euro 能源问题energy problems 能源利用率energy efficiency 能源结构energy resource structure 高价差high prize difference 联合国开发计划署 UNDP 减排市场emissions market 氟利昂freon 钢铁公司iron company 新日铁公司Nippon steel 三菱Mitsubishi 哥本哈根世界气候大会 world climate conference in Copenhagen

Australiantaxationlawnotes澳大利亚税法概要

Topic 2 Ordinary Income 1.Assessable income = ordinary income + statutory income (s. 6-1(1)) Taxable income = assessable income - deduction (s. 995-1(1) & s. 4-15) 2.Ordinary income: a. Periodicity, recurrence & regularity (Harris, Dixon) b. Income must be money or convertible into money c. Receipts from income producing activities will be regarded as ordinary income & income earning activity (Harris, Dixon) 3.Income earning activities: a. Personal exertion (personal services, employment, one-off services) b. Property (interest, rent, dividend) c. Carrying on a business (sales, services) 4.S. 21A enables value of benefit, non-cash benefit, to be assessed as ordinary income under s. 6- 5. FCT v Cooke & Sherden 5.S.21A does not operate in an employment relationship. If employment, the benefit is taxed under FBT. 6.Non-cash benefit: property or services provided wholly or partly in respect of a business relationship, or for or in relation directly or indirectly to a business relationship. S. 21A(5) 7.S. 21A(3): the value of the benefit is reduced to the extent that the taxpayer would have been entitled to a once only deduction if the taxpayer had incurred the cost. 8. Entertainment is non-deductible per s. 32-5. 9. If a receipt is ordinary income under s. 6-5, a receipt that substitutes for it will also be ordinary income under s. 6-5. FCT v Dixon 10.Receipts generally not considered as ordinary income include capital, windfall gains, hobby receipts and mutual receipts. 11.Purely gift from friend or family cannot be treated as ordinary income. FCT v Harris 12.The compensation for the cancellation of business contracts is income. Heavy Minerals Pty Ltd v FCT 13.Amount received for the sterilisation of assets are treated as capital (loss of use of asset or income producing capacity). Glenboig Union Fireclay Co Ltd v IRC

我国个人所得税存在的问题及改进意见

我国个人所得税存在的问题及改进意见 摘要: 我国个人所得税订立太晚,个人所得税法在修订后的使用过程中,不断暴露出一些问题与不足。存在着税制不完善、公民纳税意识薄弱、执法不严、征收范围不全面、征收管理力度不足、起不到应有的调节收入分配作用等问题,导致税款过多流失。故而完善我国个人所得税制,让它更加规范化,符合国际惯例,同时建立科学、合理、严密、有效的税收征管制度,是市场经济发展的必然趋势,也是当下我国经济发展的重要进程。 关键词:个人所得税;存在问题;改进意见 引言:个人所得税是国家对本国公民、居住在本国境内的个人的所得和境外个人来源于本国的所得征收的一种所得税。在有些国家,个人所得税是主体税种,在财政收入中占较大比重,对经济亦有较大影响。个人所得税是一个世界性的重要税种,全世界22个发达国家,17个国家以此税种为主,剩余国家个人所得税税收占税收收入的比例最低的也在14%以上,尤其是发展中国家,个人所得税在聚集财政收入,调控收入分配,调节经济发展方面发挥出了巨大的作用。随着经济全球化的发展,跨国人才流动日趋频繁,跨国所得不断增多,国内居民收入来源也更加多样化。面对新形势,我国现行个人所得税制难以适应,必须进一步完善和优化。 1、我国现行个人所得税存在的问题 我国于1980年开始征收个人所得税,1994年实施了个人所得税制改革,随历经9次修改,个人所得税收入呈逐年增长的趋势,个人所得税在调节个人收入、缓解社会分配不均、增加国家财政收入方面起了较大的作用。但从整体情况看,个人所得税税款流失严重,其调节力度还鞭长莫及。导致这种局面最主要原因是我国现行的个人所得税仍有诸多不完善之处。 1.1、征收范围不全面 个人所得税在课税范围的设计上,可分为概括法和列举法。概括法即按课税客体的类别设置,列举法即按课税客体的具体项目分别设置。列举法又可以分为正列举方式和反列举方式。正列举方式即对税法中有确切订立的项目给予课税,尚未出现在税目中的项目不用纳税。反列举方式则是确切规定出不在纳税范围的项目,除此之外所有项目都要纳税。通常地,反

国际碳信息披露的现状及我国碳信息披露的路径选择

第31卷 第1期 2016 年 2月 齐 鲁 师 范 学 院 学 报 Vol. 31 No. 1 Feb. 2016 Journal of Q ilu Normal University 摘要:碳排放量的增加导致全球气候变暖和生态系统被破环,碳信息披露已备受各方关注。英国、美国和澳大利亚等国已颁布了强制性碳信息披露法律,许多国际组织也发布了自愿性碳信息披露标准。但目前碳信息披露存在缺乏可比性、尚未融入主流财务报告框架、碳信息的供给与需求未能建立有效对接等不足之处。随着低碳经济的发展和碳交易机制的健全,我国应加强碳信息披露的法律法规建设,统一碳信息披露标准,实行自愿与强制相结合的披露模式,将碳信息披露融入主流财务报告框架中,构建政府、第三方鉴证机构、企业“三位一体”的碳信息披露监管机制,以满足利益相关者的决策需要。 关键词:碳信息;披露标准;财务报告;监管机制 中图分类号:X169 文献标识码:A 文章编号:2095 - 4735(2016)01 - 0099 - 07 为了应对全球气候变暖问题,联合国政府间气候变化专门委员会(IPCC)于1992年6月就气候变化问题达成公约,签署了《联合国气候变化框架公约》(UNFCCC),明确各国在碳减排和面对气候变化问题应负担的责任,为国际间开展碳减排合作提供了一个基本框架。此后UNFCCC 缔约方先后在东京、哥本哈根、德班召开会议,达成一系列协议,共同应对气候变化带来的不利影响。为了履行碳减排义务,美国、欧盟等纷纷建立碳交易市场,实施碳交易机制,如芝加哥气候交易所(CCX)、欧盟排放交易机制(EU-ETS)等。我国是以煤碳为主的能源消费国之一,快速的经济增长和以煤碳为主的能源消费结构导致碳排放量呈现明显的增长态势。作为一个负责任的发展 中国家,我国政府在哥本哈根联合国气候大会上承诺,截止2020年我国单位GDP 的碳排放量较2005年降低40%-50%。从2008年开始,我国先后建立了北京环境交易所、天津排放权交易所和上海环境能源交易所等10多家碳交易平台,对碳交易运作和交易机制进行了有益的尝试。[1](32-38)随着国际气候公约的演进以及碳交易市场的运行,碳交易过程中所产生的碳资产与碳负债、碳收入与碳费用等会计要素的确认与计量自然成为会计信息系统的重要组成部分,碳信息披露已成为备受各方关注的焦点。 一、国际碳信息披露现状(一)强制性碳信息披露1.英国强制性碳信息披露 收稿日期:2015-10-15 基金项目:福建省中青年教师教育科研A 类项目(项目批准号:JAS14416)。作者简介:陈秀霞(1966—),女,福建仙游县人,教授,硕士。 国际碳信息披露的现状及我国碳信息披露的路径选择 陈秀霞 (福建商业高等专科学校 会计系, 福建 福州 350012 )

澳大利亚税收制度概况

一、澳大利亚税收制度概况 澳大利亚为联邦制国家,行政管理分联邦、州、地方三级政府,全国划分为6个州和两个地区。实行行政、立法和司法三权分立,其行政事务由内阁负责,内阁由总理主持。联邦国会是国家的立法机构。议会实行两院制,即众议院和参议院。各级政府行政管理层次分明,联邦政府主要负责国防、外交、贸易、大学教育、福利、就业、社会保险、州际基础设施等事务;州政府主要负责中小学教育、医疗卫生、福利、交通运输、公共秩序与安全、环境、财政、城市供水、州内基础设施等事务;地方政府主要负责废物管理、产妇医疗保健、公园和花园、地方道路、其他市政。 澳大利亚实行分税制,税收收入分为联邦税收收入和地方税收收入两类,其联邦、州和地方三级政府分别对应了三级税收权限。 澳大利亚政府从20世纪80年代中期开始,对其税收制度进行改革。1985—1996年,工党政府对税收政策进行了局部调整;从1996年后,进入全面税制改革阶段。为了提高政府收入水平,缓解所得税税负过重给纳税人造成的压力,协调直接税与间接税之间的比例关系,同时抵消地下经济和灰色收入造成的负面影响,澳大利亚于2000年7月对原有税制进行了结构性改革。经过改革后,主要税种有个人所得税、公司所得税、商品与劳务税、退休金税、国民保健税、福利税、资源税、关税、土地税、印花税、消费税、工薪税、机动车辆税、资源特许权使用税、银行账户税等。 按照分税制财政体制,税种在各级政府间的划分如下: 表一:澳大利亚政府间税种划分

联邦政府 州政府 地方政府 个人所得税 土地税 相关收费, 如垃圾费和水电气等服务性收费。 公司所得税 印花税 商品与劳务税 消费税 退休金税 工薪税 国民保健税 机动车辆税 福利税 资源特许权使用税 资源税 银行账户税 关税 (一)个人所得税 目前,澳大利亚对个人所得税实行五级超额累进税率, 2006至2007纳税年度的居民个人所得税税率如下表: 表二:2007纳税年度的居民个人所得税税率表 级数 全年应纳税所得额(澳元) 税率(%) 1 6,000以下 0 2 超过6,001至25,000的部分 15% 3 超过25,001至75,000的部分 30% 4 超过75,001至150,000的部分 40% 5 超过150,000的部分 45% (二)公司所得税

1个人所得税生产经营所得纳税申报表(A表)

附件1 个人所得税生产经营所得纳税申报表(A 表) 税款所属期: 年 月 日至 年 月 日 金额单位:人民币元(列至角分) 国家税务总局监制 投资者信息 姓 名 身份证件类型 身份证件号码 国籍(地区) 纳税人识别号 被投资单位 信息 名 称 纳税人识别号 类 型 □个体工商户 □承包、承租经营单位 □个人独资企业 □合伙企业 征收方式 □查账征收(据实预缴) □查账征收(按上年应纳税所得额预缴) □核定应税所得率征收 □核定应纳税所得额征收 □税务机关认可的其他方式 行次 项 目 金 额 1 一、收入总额 2 二、成本费用 3 三、利润总额 4 四、弥补以前年度亏损 5 五、合伙企业合伙人分配比例(%) 6 六、投资者减除费用 7 七、应税所得率(%) 8 八、应纳税所得额 9 九、税率(%) 10 十、速算扣除数 11 十一、应纳税额(8×9-10) 12 十二、减免税额(附报《个人所得税减免税事项报告表》) 13 十三、已预缴税额 14 十四、应补(退)税额(11-12-13) 谨声明:此表是根据《中华人民共和国个人所得税法》及有关法律法规规定填写的,是真实的、完整的、可靠的。 纳税人签字: 年 月 日 感谢您对税收工作的支持! 代理申报机构(负责人)签章: 经办人: 经办人执业证件号码: 代理申报日期: 年 月 日 主管税务机关印章: 受理人: 受理日期: 年 月 日

《个人所得税生产经营所得纳税申报表(A表)》填报说明 本表适用于个体工商户、企事业单位承包承租经营者、个人独资企业投资者和合伙企业合伙人在中国境内取得“个体工商户的生产、经营所得”或“对企事业单位的承包经营、承租经营所得”的个人所得税月度(季度)纳税申报。 合伙企业有两个或两个以上自然人合伙人的,应分别填报本表。 一、申报期限 实行查账征收的个体工商户、个人独资企业、合伙企业,纳税人应在次月(季)十五日内办理预缴纳税申报;企事业单位承包承租经营者如果在1年内按月或分次取得承包经营、承租经营所得的,纳税人应在每月或每次取得所得后的十五日内办理预缴纳税申报。 实行核定征收的,纳税人应在次月(季)十五日内办理纳税申报。 纳税人不能按规定期限办理纳税申报的,应当按照《中华人民共和国税收征收管理法》及其实施细则的规定办理延期申报。 二、有关项目填报说明 (一)表头项目 税款所属期:填写纳税人自本年度开始生产经营之日起截至本月最后1日的时间。 (二)表内信息栏 1.投资者信息栏 填写个体工商户、企事业单位承包承租经营者、个人独资企业投资者和合伙企业合伙人的相关信息。 (1)姓名:填写纳税人姓名。中国境内无住所个人,其姓名应当用中、外文同时填写。 (2)身份证件类型:填写能识别纳税人唯一身份的有效证照名称。 (3)身份证件号码:填写纳税人身份证件上的号码。 (4)国籍(地区):填写纳税人的国籍或者地区。 (5)纳税人识别号:填写税务机关赋予的纳税人识别号。 2.被投资单位信息栏 (1)名称:填写税务机关核发的被投资单位税务登记证载明的被投资单位全称。 (2)纳税人识别号:填写税务机关核发的被投资单位税务登记证号码。 (3)类型:纳税人根据自身情况在对应框内打“√”。 (4)征收方式:根据税务机关核定的征收方式,在对应框内打“√”。采用税务机关认可的其他方式的,应在下划线填写具体征收方式。 (三)表内各行的填写 1.第1行“收入总额”:填写本年度开始生产经营月份起截至本期从事生产经营以及与生产经营有关的活动取得的货币形式和非货币形式的各项收入总金额。包括:销售货物收入、提供劳务收入、转让财产收入、利息收入、租金收入、接受捐赠收入、其他收入。 2.第2行“成本费用”:填写本年度开始生产经营月份起截至本期实际发生的成本、费用、税金、损失及其他支出的总额。 3.第3行“利润总额”:填写本年度开始生产经营月份起截至本期的利润总额。 4.第4行“弥补以前年度亏损”:填写可在税前弥补的以前年度尚未弥补的亏损额。 5.第5行“合伙企业合伙人分配比例”:纳税人为合伙企业合伙人的,填写本栏;其他则不填。分配比例按照合伙协议约定的比例填写;合伙协议未约定或不明确的,按合伙人协商决定的比例填写;协商不成的,按合伙人实缴出资比例填写;无法确定出资比例的,按合伙人平均分配。 6.第6行“投资者减除费用”:填写根据实际经营期限计算的可在税前扣除的投资者本人的生计减除费用。 7.第7行“应税所得率”:按核定应税所得率方式纳税的纳税人,填写税务机关确定的核定征收应税所得率。按其他方式纳税的纳税人不填本行。 8.第8行“应纳税所得额”:根据下表对应的方式填写。

2015我国个人所得税的制度缺陷及改革思路_利雅

036 吉林省经济管理干部学院学报 2015年6月 Journal of Jilin Province Economic Management Cadre College 收稿日期:2015-03-01 作者简介:利 雅(1987-),女,汉族,广东省梅州市人,广州工商学院财金信息管理系思想政治辅导员。研究方向:财税教学及学生教育管理。 我国个人所得税的制度缺陷及改革思路 利 雅 (广州工商学院, 广东 广州 510850) 摘 要:我国的个人所得税制度在税制模式、税率与税制设计、征收管理等方面存在着缺陷和漏洞,一定程度上削弱了税收对收入公平调节的作用。应该从科学优化税制模式、合理调整税率结构和提高税务机关的税收征管水平等方面入手,逐步完善我国个人所得税制度。 关 键 词:个人所得税 ; 税制模式 ; 税率与税制设计 ; 税收征管中图分类号:F812.42 文献标识码:A 文章编号:1009-0657(2015)03-0036-03 以个人(自然人)取得的应税所得为征税对象所征收的税,叫个人所得税。我国首次对个人所得开征个人所得税,是1980年9月第五届全国人民代表大会第三次会议公布的《中华人民共和国个人所得税法》。开征以来,个人所得税通过了六次修改,目前执行的是2011年6月修订并从当年9月1日起开始实施的《中华人民共和国个人所得税法》。 个人所得的来源非常广泛,包括所有的工资薪金所得、劳务报酬所得、稿酬所得、个体工商户生产经营所得、企事业单位的承包承租经营所得、特许权使用费所得、财产租赁所得、财产转让所得、利息股息红利所得、偶然所得等;以及除以上各项所得以外的,其他确实有必要征收的,由国务院财政部门确定的个人所得;还包括一些难于界定应纳税所得项目的,由主管税务机关进行确定的个人所得。总之,各项所得均须视情况缴纳个人所得税,我们每个人都有可能成为个人所得税的纳税人。我国个人所得税采用的是分类课征制,这是我国目前个人所得税的特点之一,即不同所得按照对应的税率、费用扣除和计税的方法来征税。 一、分类课征税制模式存在缺陷,需科学优化我国个人所得税目前选择的是分类课征的税制 模式,即将纳税人不同性质和来源的所得项目,分别按照超额累进税率和比率税率两种税率形式进行征税。累进税率与比例税率并用,是我国目前个人所得税的特点,而采用源泉扣缴并且操作简单方便,则是分类课征税制模式的显著特点。随着经济的发展,分类课征税制模式的缺陷逐渐显现出来,目前已无法实现个人所得税对收入进行公平调节的目的。主要表现在:第一,税源流失。收入来源种类日益多样化,这将扩大个人所得税计税依据或计税标准的范围,导致现有应税项目无法囊括全部收入种类。我国现行税制中,不同来源收入征收所得税的税率和扣除额不完全相同,容易出现两种情况:一是纳税人可以进行收入类型转换,把税率高的应税项目转移到税率低的应税项目,或把收入由扣除额低的项目向扣除额高的项目转移,以达到少缴税或不缴税的目的。二是纳税人单项收入有可能无需纳税或少纳税,结果造成税源流失,无法实现个人所得税对收入进行公平调节的目的。第二,税负不公。现行税制下,不同的纳税人即便收入相同,但因为收入来源不一,应按不同的所得项目计征个税,采用的费用扣除标准和适用税率不同,其结果是收入相同,但税收负担并不一样。第三,调节收入力度不足。在现行税制下,个人所得税以自然人为

澳大利亚财政管理体制及启示

澳大利亚财政管理体制及启示 一、澳大利亚国情概况 澳大利亚地处南半球,土地面积768万平方公里,是世界第六大面积国家,也是唯一一个领土覆盖整个大陆的国家。澳大利亚是一个多元文化国家,人口约2000万,是世界上人口密度最小的国家,资源丰富,农牧业及服务业都很发达。它的领土划分为六个州和两个领地:分别是新南威尔士州、维多利亚州、昆士兰州、南澳大利亚洲、西澳大利亚洲、塔斯马尼亚洲和北领地、首领地(即首都堪培拉所在地,人口约32万)。 澳洲原为土著人居住,后成为英国殖民地,1901年形成澳大利亚联邦,只有100多年的建国史。由于上述历史渊源的因素,澳大利亚类似英美模式。其政治体制实际上是非完全意义的三权分立。议会是国家立法机构(包括参议院和众议院),负责制定法律,澳大利亚的法律体系很健全。宪法第83款规定,没有法律对拨款的授权,任何资金都不能从联邦中支出。由此看出国家财政资金是由议会控制的。总督是国家元首,由英国女王任命,负责签发议会通过的法案。总督一般没什么实权,但其能够任免总理。行政机关的总理和部长(即内阁)是议会的成员,而且总是从下议院多数派政党中选举出来的。这一点澳大利亚宪法遵循了英国的责任政府模式。这种模式不同于美国,美国总统由人民选举产生,而不是议会成员。同样,总统的部长也从议会外任命。由此看出,其行政机关与立法机关不是完全分离,特别是2005年7月1日后以霍华德为领袖的自由党多年来首次控制了参众两院,更削弱了两权的独立性。澳大利亚主要党派有自由党、工党、国民党和绿党。司法机构包括警察和各级法院,它们对于政府是独立的。 二、澳大利亚的财政管理体制

(一)澳大利亚政府间的事权划分明确 澳大利亚的公共行政管理系统主要沿袭英美模式。国家行政管理分为联邦、州(6个州和2个领地)和地方(约863个)三级。每个州有各自的体制,负责管理地方政府,都具有很大的独立性。与政府分级管理相适应,澳大利亚实行典型的分税、分级财政管理体制,并通过较为规范的财政转移支付制度,尽可能使公民享受均等的社会公共服务。各级政府间事权划分非常明确。 涉及全国的事物由联邦负责,主要有:国防、外交、宏观经济管理、全国性的税收、州际基础设施、电讯、移民、金融、社会保险;涉及州内的公共产品和服务由州一级政府提供,主要有教育、警察、卫生、医疗保健、交通和州内的社会经济基础设施;地方政府只负责一些非常本地化的事物,如:社区服务、消费

我国个人所得税现状及改革

摘要:摘要随着居民收入水平的提高,我国个人所得税收入在财政收入规模中的比重也在逐年提高。各地税务机关开展了纳税人自行申个人所得税的工作,完善了全员全额扣缴申治理,有效地堵塞了税收漏洞,抑制了偷漏税现象,促进了个人所得税收入的提高。个人所得税征管工作中还存在一些问题,对此,应当针对造成问题的原因采取相应的对策。2011年 6月的最后一天,十一届全国人大常委会第二十一次会议表决通过了关于修改个人所得税法的决定,个税起征点上调到3500元。修改后的个税法将于9月1日起施行。 一、我国个人所得税的概况 据国家税务总局的数据,1994年中国个人所得税收入仅为72.7亿元,2004年达到1737.05亿元,十年提高了约24倍;占中国税收总收入的比重也从1994年的1.4%,迅速提升至2004年的6.75%,个人所得税已成为中国第四大税种和中国财政收入的一项重要来源。近日,社会各界期盼已久的个人所得税法(修订)立法进程,正在按照人大立法计划如期进行,修改方案已经在8月23日由国务院提请人大常委会第十七次会议审议,从而进入人大立法的“一读”程序。 我国所得税制是1980年制定的,尽管中间有几次小的调整,但是我国现行税制的第一个重要的弊端就是起征点多年不变。第二个弊端就是个人所得税的模式选择问题。大多数发达国家都选择一个综合所得税制模式,而中国选择的是一个分类所得税制模式。分类所得税制的一个重要缺陷在于处于同一收入水平的纳税人的纳税负担不相同。由于收入来源不同,最后的实际税收负担也不相同。此外,我国现行所得税制没有考虑一些个案,比如同样的收入水平,个人身体健康状况不一样,表面上看,纳同样的税好像很公平,但是这个纳税之后的生活负担能力或者承受能力可能截然不同。 目前国个税最大的弊端在于现行税制没有体现公平税负,合理负担的原则,没有起到调节社会公平应有的作用。首先,工薪阶层税负过重。如今国工薪阶层月薪3000元-5000元里面增加了很多的支出容,如住房公积、医疗支出、教育费用、养老保障,这部分月薪实际上对许多工薪阶层仅够维持生计用,但目前税制仍然按照富人的标准来对他们征税。其次就是调节的重点对象有失偏颇。中低

澳大利亚碳税立法及其影响_陈晖

电力与能源第33卷第1期 2012年2月澳大利亚碳税立法及其影响 陈 晖 (上海图书馆上海科学技术情报研究所,上海 200031) 摘 要:介绍了澳大利亚碳排放的现状,清洁能源法案的背景,包括澳大利亚各政党、各利益集团围绕碳税立法的角力过程,以及澳大利亚碳税立法,包括碳税的定价机制、征收对象以及政府为了顺利实施清洁能源法案所采取的一系列配套措施。分析了实施碳税立法后,可能给澳大利亚企业经营、国民经济发展、能源结构调整以及对国际减排合作和全球碳市场发展带来影响。澳大利亚碳税立法将有力推动本国的可再生能源、清洁能源和节能技术的进步和产业的发展,对全球经济向低碳转型具有积极的示范意义。 关键词:澳大利亚;碳税;碳机制;碳排量;碳税立法 中图分类号:F062.2 文献标志码:C 文章编号:2095-1256(2012)01-0006-04 Carbon Price Legislation in Australia and Its Impacts Chen Hui (Shanghai Library &ISTIS,Shanghai 200031,China) 2011年11月28日至12月9日,联合国气候变化框架公约(UNFCCC)第17次缔约方会议(COP17)在南非德班召开,会议的目的是为《京都议定书》第二承诺期的存续问题寻求解决方案。会议虽然取得了一些成果,但是与会各国还存在许多分歧,全球性气候问题的解决任重道远。经过多年来全球减排碳的合作实践,各国政府都已认识到,为了实现在国际社会中作出的减排承诺,除了调整本国的经济发展外,利用和推广《京都议定书》引入的市场机制也是一个非常有效的手段,开征排碳税就是对这种市场机制的一种创新。2011年11月8日澳大利亚参议院通过的清洁能源法,以碳税(碳定价机制)的立法为核心和基础,对澳大利亚未来清洁能源的发展进行了规划。作为继欧盟之后开征排碳税的第二大经济体的澳大利亚,在COP17召开的前夕确立碳税制度的意义重大,受到各国的关注。本文拟就澳大利亚碳税立法的基本情况和立法内容作一介绍,并且对其意义及后续影响作简要评析。 1 立法的背景 澳大利亚是一个发达国家,根据经济合作与发展组织(OECD)2011年的统计数据,2010年澳大利亚的国内生产总值(以即期购买力平价计算)约为9 166亿美元,全球排名第13位;2008年人均收入 为36 897美元,全球排名第10位。根据联合国《2011年人类发展报告》统计数据,澳大利亚的人类发展指数(HDI)列全球第2位,仅次于挪威。 澳大利亚也是一个碳排放大国,据国际能源署(IEA,2010)公布的数据,2008年澳大利亚因燃料产生的二氧化碳排放总量为3.98亿t(占全球碳排放的比例为1.35%),列全球第12位。与一些碳排放大国相比,澳大利亚的碳排放总量不算太大,但是人均碳排量强度很高,2006年澳大利亚人均年碳排量为26.7t,居全球第一。表1是根据IEA,UNFCCC和Population ReferenceBureau公布的数据计算的OECD中人均碳排量强度最高的几个国家在2005年和2006年的碳排放情况。 表1 人均二氧化碳年排放量t国 家2005年2006年 澳大利亚30.3 26.0 美国24.5 23.5 卢森堡24.0 26.6 新西兰22.6 19.0 加拿大22.5 22.1 爱尔兰15.6 16.6 捷克共和国14.3 14.4 澳大利亚的温室气体来源的分布见图1(资料来源:University of Melbourne Energy Re-search Institute,“Australian Sustainable EnergyZCA2020Stationary Energy Plan”(Second edi- 6

澳大利亚税收居民身份认定规则-国家税务总局

澳大利亚税收居民身份认定规则 一、个人 为协助个人(包括已进入或离开澳大利亚的个人)认定其自身是否为澳大利亚税收居民,澳大利亚税务局(ATO)发布了在线指南1及计算工具1。 一般情况下,判定个人是否为澳大利亚税收居民依据普通法和成文法并结合该人具体情况确定。例如,一个纳税年度内在澳大利亚居住时间超过一半的个人很可能构成澳大利亚税收居民。 个人如果由于情况复杂等原因,在认定澳大利亚税收居民身份方面需要进一步帮助,应咨询税务顾问或联系澳大利亚税务局2。 普通法认定 根据“居住”一词的本义(1936所得税评估法案第6(1)章节3),澳大利亚税收居民是指在澳大利亚“居住”的个人。一般而言,居住概念需要考虑个人在相应纳税年度的整体情况,包括: 停留在澳大利亚境内的意图或目的 1 https://https://www.360docs.net/doc/6a9714773.html,.au/Individuals/International-tax-for-individuals/Work-out-your-tax-residency/?anc hor=P14_2083#P14_2083, https://https://www.360docs.net/doc/6a9714773.html,.au/Calculators-and-tools/Are-you-a-resident/ 2https://https://www.360docs.net/doc/6a9714773.html,.au/About-ATO/About-us/Contact-us/ 3https://www.360docs.net/doc/6a9714773.html,.au/au/legis/cth/consol_act/itaa1936240/s6.html

?家庭、经营活动和就业与澳大利亚的关联程度 ?个人资产所在地和维护情况 ?社会和生活安排 税务裁定98/174提供了澳大利亚税务局局长依据1936所得税评估法案第6(1)章节对“居住”一词在一般意义上的解读5。 成文法认定 如个人不满足普通法对于居住的认定,但符合1936所得税评估法案第6(1)章节陈述的以下三条成文法认定中的任一条,仍应被认定为澳大利亚税收居民6: ?其住所/永久性居住地位于澳大利亚的个人(永久性居住地不在澳大利亚境内的除外) ?其在一个纳税年度内在澳大利亚境内实际停留时间超过一半的个人(习惯性住所不在澳大利亚境内的除 外) ?缴纳联邦政府公务员养老金的个人(包括其配偶及16岁以下的孩子)。 此外,还有一种个人为澳大利亚临时税收居民的情形(temporary Australian resident)。这种情况通常为个人持有澳大利亚临时居民签证,可以进入澳大利亚境内并在限定的时 4https://www.360docs.net/doc/6a9714773.html,.au/pdf/pbr/tr1998-017.pdf 5https://www.360docs.net/doc/6a9714773.html,.au/au/legis/cth/consol_act/itaa1936240/s6.html 6https://www.360docs.net/doc/6a9714773.html,.au/au/legis/cth/consol_act/itaa1936240/s6.html

经营所得个人所得税缴款指引

2019年经营所得个人所得税缴款指引 2019年度经营所得个人所得税(不包括定期定额户)缴款发生变化,请关注: 1.需由自然人纳税人个人完成缴款。 2.目前提供个人三方协议和银联卡两种在线缴款模式。特别提醒,自然税收管理系统WEB端与扣缴客户端缴款模式略有不同。 3.请提前做好三方协议签订、银联卡支付等相关准备工作;尽早完成经营所得申报缴款。 自然人税收管理系统WEB端 特别提醒,WEB端申报可以在WEB端完成缴款;扣缴客户端申报后未缴款的,也可以在WEB端完成缴款。WEB端支持个人三方协议和银联卡两种在线缴款模式,同时支持在线打印电子缴款凭证至银行缴款。 一、三方协议缴税 本功能适用于已签订三方协议的纳税人在缴款时进行选择。 操作步骤: 1.点击【申报管理】-【已申报】-【未完成】,选择对应申报项目进行缴税,如有多条未缴款记录可点击【立即缴

税】(仅同一个税款所属机关、收款国库的申报可合并缴税); 2.支付方式选择【三方协议缴款】,点击【立即支付】; 3.确认此次缴税所使用的三方协议缴款账户,点击【确定】发起扣款请求完成缴税。

二、银联在线支付 未签订三方协议缴款的纳税人,可选择银联在线支付完成缴款。 操作步骤: 1.点击【申报管理】-【已申报】-【未完成】,选择对应申报项目进行缴税,如有多条未缴款记录可点击【立即缴税】(仅同一个税款所属机关、收款国库的申报可合并缴税); 2.支付方式选择【银联在线支付】,点击【立即支付】;

3.选择直接付款或者登录付款,发起扣款请求完成缴税。 特别提醒:怎么查询已缴税情况? 点击【申报管理】-【已申报】-【已完成】,纳税人可查看已缴税情况。